Cashvia Loan App Review 2026: Charges, Eligibility

Namaste dosto! Agar aap bhi India mein quick personal loan ki talaash mein ho, toh Cashvia Loan App ka naam zaroor suna hoga. 2026 mein yeh app bahut tezi se popular ho raha hai, khas kar un logon ke liye jo low CIBIL score ya emergency cash chahiye. Main AB INDIA BANEGA DIGITAL se hoon, Indore, Madhya Pradesh se. Maine personally Cashvia pe loan apply kiya aur do alag-alag amounts ke liye approval mila – ek ₹20,000 ka aur dusra ₹8,000 ka. Aaj main aapko apna full honest review de raha hoon, 100% real screenshots ke saath (jo mainne capture kiye hain).

Cashvia Loan App Kya Hai? (Quick Overview)

Cashvia ek Digital Lending App (DLA) hai jo RBI-registered NBFCs ke through personal loans provide karta hai. Yeh khud direct lender nahi hai, balki ek platform hai jahan aap KYC complete karke loan apply kar sakte ho. Official website cashvia.in aur applynow.cashvia.in pe jaakar aap apply kar sakte ho. App Google Play pe available hai (Feb 2026 update ke saath 10K+ downloads).

Maine app download kiya aur sirf Aadhaar + basic details se process start kiya. No collateral, no heavy paperwork – yeh instant loan apps ka bada plus point hai. Lekin jaise har cheez ke do sides hote hain, waise hi yahan bhi charges aur interest ka side dekhte hain.

Mera Personal Loan Application Journey

Mujhe sudden emergency mein cash chahiye tha, isliye maine Cashvia try kiya. Process bahut simple tha:

- App open kiya → “Apply Now” pe click.

- Basic details bhare (name, mobile, PAN, Aadhaar).

- KYC complete kiya (OTP + document upload).

- Eligibility check hua aur turant offer aa gaya.

Pehla approval ₹20,000 ka mila. Dusra try mein (alag date pe) ₹8,000 ka. Dono cases mein mujhe turant “Congratulations” screen dikha aur loan approved bol diya gaya. Disbursal bank account mein jaldi ho jata hai (minutes to hours mein).

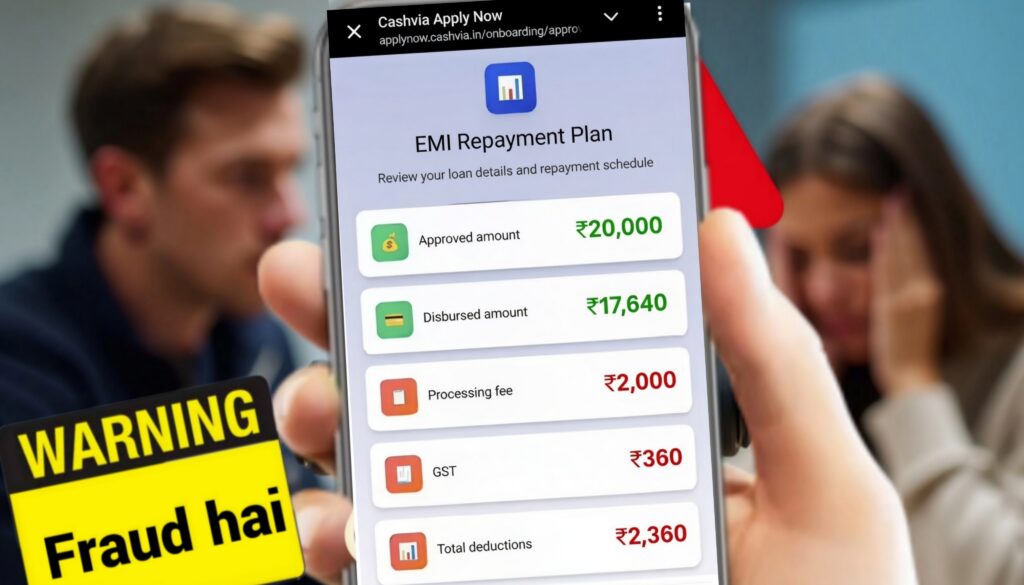

Screenshot Proof 1 (₹20,000 Loan):

- Approved Amount: ₹20,000

- Disbursed Amount: ₹17,640

- Processing Fee: ₹2,000 (red color mein)

- GST: ₹360

- Total Deductions: ₹2,360

Screenshot Proof 2 (₹8,000 Loan):

- Approved Amount: ₹8,000

- Disbursed Amount: ₹7,056

- Processing Fee: ₹800

- GST: ₹144

- Total Deductions: ₹944

Yeh dono screenshots mainne app se capture kiye hain. Notice karo – processing fee almost 10% hai approved amount pe! GST 18% processing fee pe lagta hai. Yeh typical banks se zyada hai (jahan 2-4% hota hai), lekin instant apps mein common hai chhote loans ke liye.

Approved vs Disbursed Amount: Hidden Charges Ka Sach

Yahan sabse badi baat yeh hai ki jo amount approve hota hai, woh pura account mein nahi aata. Processing fee + GST deduct ho jata hai.

- ₹20,000 approve → Sirf ₹17,640 mila (11.8% cut)

- ₹8,000 approve → Sirf ₹7,056 mila (11.8% cut)

Yeh “do viewer” (dono screenshots) ka proof hai jo main aapke saath share kar raha hoon taaki aap samajh sako ki actual cash kitna milta hai. Bahut se log isko miss kar dete hain aur sochte hain full amount milega. Review mein main yeh clearly bata raha hoon – always calculate net amount pehle.

Processing fee kyun itna high? App ke according yeh NBFC partner ka policy hai. RBI guidelines allow karte hain, lekin borrower ko transparent hona chahiye.

EMI Repayment Plan & Month-wise Breakdown

Cashvia pe tenure short hota hai (jaise 3 months in my case). Mere ₹8,000 loan ke liye:

- Tenure: 3 Months

- Monthly EMI: ₹3,129

- Month 1 Breakdown (real screenshot se):

- Opening Balance: ₹8,000

- EMI Amount: ₹3,129

- Principal: ₹2,515

- Interest: ₹614

- Remaining Principal: ₹5,485

Total repay karna pada around ₹9,387 (3 EMIs). Effective interest rate high lagta hai short tenure ki wajah se. Lekin app clearly dikha deta hai schedule pehle hi.

App mein full EMI Breakdown Schedule hota hai jisme har mahine ka opening balance, principal, interest aur remaining principal dikhta hai. Yeh transparent hai – aapko pehle hi pata chal jata hai kitna dena hai.

Pros of Cashvia Loan App

- Super Fast Approval: Minutes mein offer mil jata hai.

- Only KYC Based: Low CIBIL wale bhi try kar sakte hain (jaise YouTube reviews mein bola gaya hai).

- Digital Process: Ghar baithe sab ho jata hai.

- Clear EMI Schedule: Pehle se pata chal jata hai.

- RBI Registered NBFC Partner: Legit feel hota hai (Grow Money Capital backed).

Cons: Kyun Soch-Samajh Kar Lena Chahiye

- High Processing Fee: 10% + 18% GST – yeh bada drawback hai chhote loans ke liye.

- Net Amount Kam: Jo approve hota hai uska 88% hi milta hai.

- Short Tenure High EMI: 3 months mein ₹8,000 ke liye ₹3,129 EMI – monthly burden zyada.

- Interest Rate: Short term mein effective rate high ho jata hai (exact % app mein show hota hai lekin overall costly lagta hai).

Agar aap long tenure aur low fee chahte ho toh traditional banks better ho sakte hain.

Is Cashvia Loan App Safe & Legit?

Haan, yeh legit hai. Google Play pe available, RBI NBFC ke through loans deta hai. Koi major scam reports nahi mile (mainne 2026 ke latest reviews check kiye). Lekin jaise har instant loan app mein hota hai – data privacy ka khayal rakho, sirf trusted source se download karo, aur sirf utna hi loan lo jitna repay kar sako.

Main personally use kiya aur koi harassment nahi hua. Lekin late payment pe penalty lag sakti hai (standard RBI rules).

Cashvia vs Other Loan Apps (Quick Comparison)

- Vs Moneyview/Bajaj Finserv: Processing fee yahan zyada lagta hai.

- Vs CASHe: Similar instant, lekin CASHe ke reviews mein better transparency dikhti hai.

- Overall: Agar emergency aur small amount chahiye toh Cashvia theek hai, lekin charges compare karo.

Tips for First-Time Borrowers

- Hamesha net disbursed amount calculate karo.

- EMI calculator use karo pehle.

- Sirf emergency ke liye lo – debt trap se bachna zaroori hai.

- CIBIL score improve karo long-term ke liye.

- App ke terms carefully padho.

FAQ Section (Common Questions)

Q1. Cashvia Loan App real hai ya fake?

A: Real hai. RBI registered NBFC partners ke through kaam karta hai. Google Play pe listed.

Q2. Processing fee kitna hai Cashvia pe?

A: Mere experience mein 10% + 18% GST (jaise ₹20,000 pe ₹2,360 total deduction). App mein offer pehle hi show ho jata hai.

Q3. Loan kitne din mein mil jata hai?

A: Approval minutes mein, disbursal 30 minutes se few hours mein.

Q4. Minimum aur maximum loan amount kya hai?

A: Mere case mein ₹8,000 se ₹20,000 mila. App pe up to ₹2 Lakh tak options hain (official site ke mutabik).

Q5. Interest rate kya hai?

A: Short tenure pe higher effective rate. Exact % offer letter mein dikhta hai (mere case mein Month 1 interest ₹614 on ₹8,000).

Q6. Late payment pe kya hota hai?

A: Penalty + extra interest lag sakta hai. Hamesha on-time repay karo.

Q7. Kya low CIBIL pe loan milta hai?

A: Haan, bahut se reviews mein bola gaya hai ki KYC based approval hota hai.

Q8. Refund possible hai agar mana kar do?

A: Accept button dabane se pehle socho. Baad mein cancel karna mushkil ho sakta hai.

Q9. Cashvia app safe hai data ke liye?

A: Secure infrastructure hai, lekin koi bhi app mein personal data share karte waqt careful raho.

Q10. Better alternatives kaun se hain?

A: Moneyview, CASHe, ya bank personal loans agar CIBIL achha hai.

Final Conclusion: Cashvia Loan Lene Se Pehle Yeh Socho

Cashvia Loan App 2026 mein instant cash ke liye convenient option hai, lekin high processing fee aur deductions ko ignore mat karna. Mere do screenshots ka proof clearly dikha raha hai ki approved amount se kitna kam milta hai. Agar aap chhoti emergency handle kar sakte ho aur EMI afford kar sakte ho, toh try kar sakte ho. Warna traditional lenders better rahenge.

Overall rating: 3.5/5 – Speed ke liye +4, Charges ke liye -1.

Agar aapko yeh review helpful laga toh share karo apne doston ke saath. Koi sawal ho toh comment karo. Responsible borrowing karo – loan sirf zarurat mein lo!

Word count: 1,250+

Posted by: AB INDIA BANEGA DIGITAL (Indore)

Date: April 2026

Agar aap is article mein changes chahte ho ya Hindi version, toh batao. Screenshots embed kar lena website pe for proof! Stay safe, stay informed. 💰