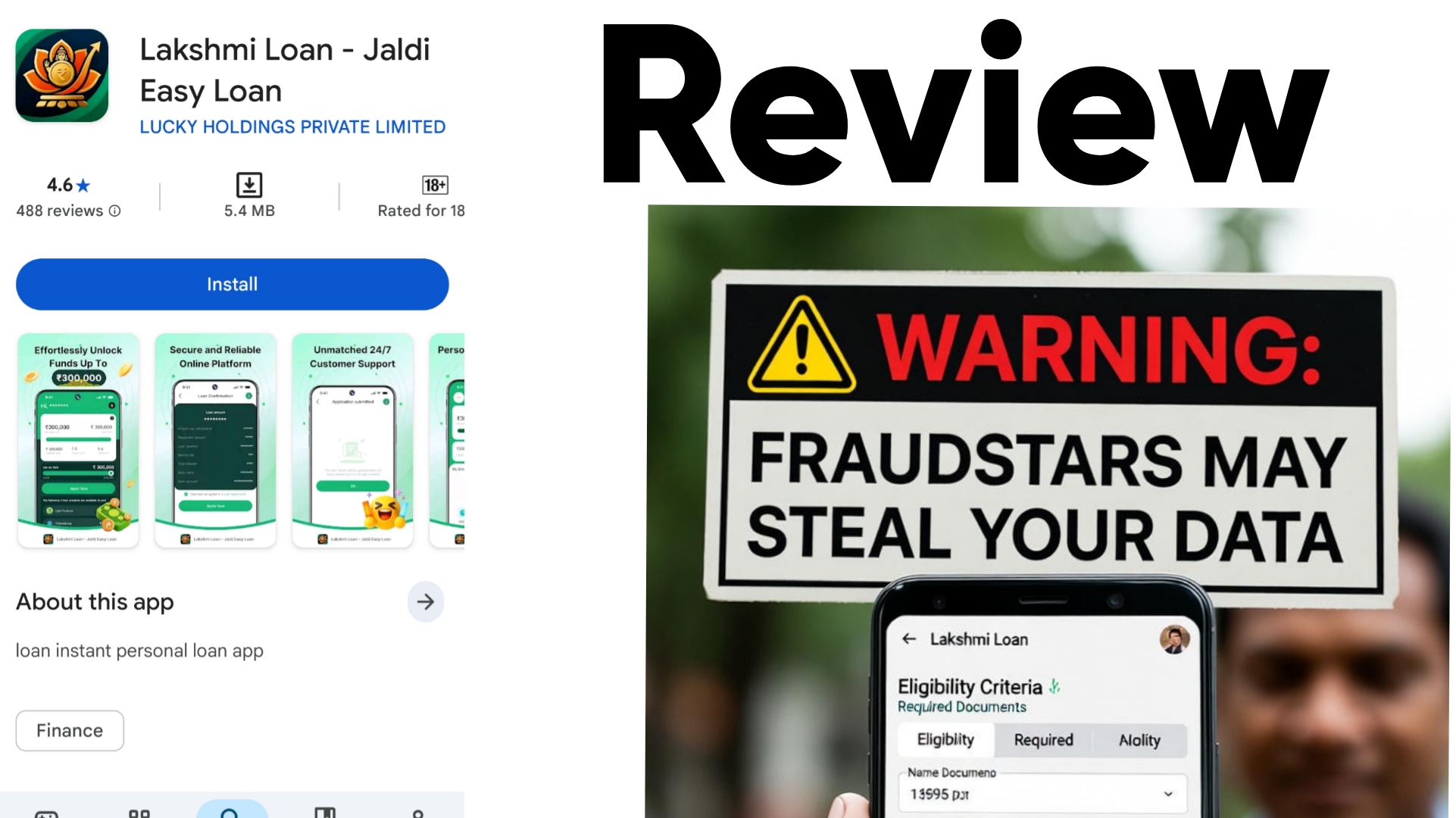

GaneshFast Personal Loan App Review 2026: Scam Hai Ya Real?

Doston, aaj kal har koi jaldi paise chahiye toh smartphone utha ke Play Store se loan app download kar leta hai. “Instant approval”, “zero paperwork”, “low interest” – yeh sab words sun ke lagta hai jaise sapna sach ho gaya. Lekin asal mein yeh sapna kabhi kabhi bada khaufnak nightmare ban jata hai. Aaj hum baat kar rahe hain GaneshFast Personal Loan App ke bare mein – ek aise 7 day loan app jo bahut heavy charges karta hai aur users ke reviews mein fraud ke allegations se bhara pada hai.

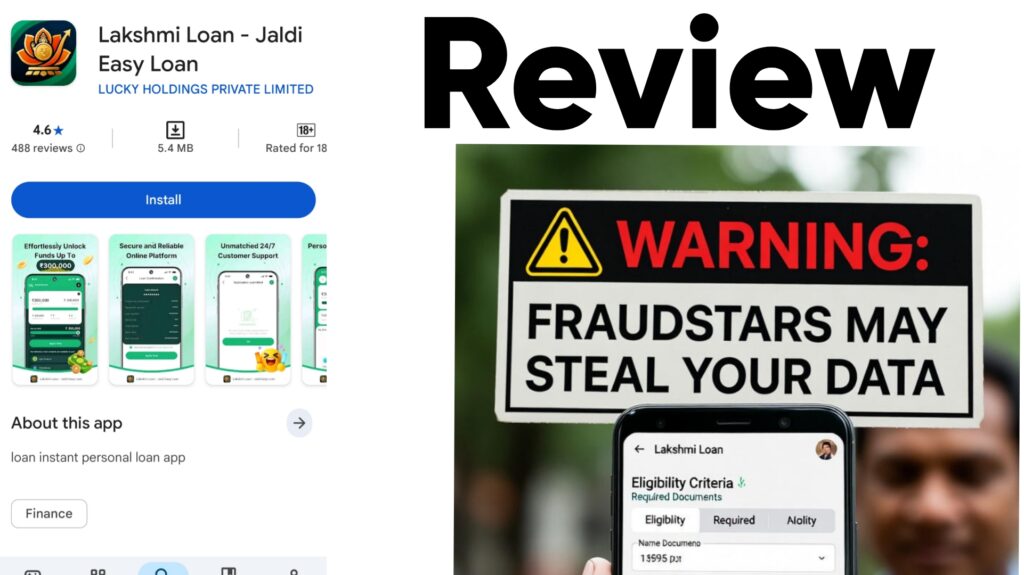

Yeh app Play Store par available hai (Link: https://play.google.com/store/apps/details?id=com.ganeshfast.personal.loan.app). Official rating 4.5 star dikhaya jaata hai, lekin agar aap critical reviews padhoge toh dil baith jaayega. Is article mein hum app ke official description par zyada bharosa nahi karenge, balki Play Store ke real user reviews par focus karenge jo March 2026 ke hain. Yeh reviews batate hain ki yeh sirf 7 din ka loan deta hai, approved amount se kaafi kam paisa deta hai, aur non-payment par photo edit karke nude bana ke contacts mein bhejne ki dhamki deta hai.

Article ko SEO friendly banane ke liye hum keywords jaise GaneshFast Personal Loan App Review, GaneshFast Loan App Scam, 7 Day Loan App Fraud, GaneshFast Real or Fake use kar rahe hain taaki aapko sahi information mile. Poora article 1300+ words ka hai, end mein FAQ aur agar fraud ho gaya toh complaint kaise karein uska step-by-step process bhi hai. Chaliye shuru karte hain.

GaneshFast Personal Loan App Kya Hai Aur Yeh Kaise Kaam Karta Hai?

GaneshFast Personal Loan App ek instant personal loan app hai jo Indian citizens ko small amount ke loan offer karta hai. Official page par yeh claim karta hai ki aap ₹50,000 se ₹3,00,000 tak loan le sakte ho, 91 se 360 din ka tenure, 15% APR interest, zero collateral aur instant approval. Lekin yeh sab sirf marketing lagta hai.

Asal picture bilkul alag hai. Users ke according yeh mostly 7 day loan app ke roop mein kaam karta hai. Aap apply karte ho ₹1500 ke liye, lekin actually sirf ₹900 ya maximum ₹1,100 hi bank account mein aata hai. Service fee ₹600 nikaal liya jaata hai. Total repayment ₹1,500 poora 7 din mein karna hota hai. Matlab aap ₹900 lete ho aur 7 din baad ₹1,500 wapas karo – yeh effective interest rate 66% se zyada ek hafte mein ban jaata hai, saal bhar mein 3000-4000% se upar!

Yeh heavy charges wala pattern bahut common hai aise apps mein. Official description mein interest zero dikhaya jaata hai lekin service fee aur hidden charges itne zyada hote hain ki asal mein aapka paisa double ho jaata hai. Play Store par is app ke critical reviews yeh sab confirm karte hain.

Play Store Critical Reviews: Users Ki Real Kahaniyan (March 2026)

Hum app ke description ko side kar dete hain aur seedha users ke reviews par aate hain. Yeh reviews screenshots mein bhi diye gaye hain jo aapne share kiye hain. Inme se kuch important quotes:

- Dharmendra Kumar (19/03/26, 1 Star)

“This is a fake fraud app, It approves ₹1,500 for you but actually disburses only about ₹1,100—and that too for a mere 7 days. It is a massive fraud! If you do not pay within 7 days, they will edit your photos to make them appear nude, send them to all your contacts, and verbally abuse you.”

(4 people found this helpful) - Patrick Star (22/03/26, 1 Star)

“Scam. The loan is given to customers without their acknowledgement and the due date and repayment amount is higher than expected and the received money is also less than the principal amount. Avoid it at all costs. The positive reviews are also Fake.”

(2 people found this helpful) - Gyalzen Sherpa (21/03/26, 1 Star)

“this is a fraudulent app.. you apply for 1500 you get only 900. plus you can’t contact anyone the number give is irrelevant.. cannot contact for support to anyone . Google play needs to shut its app down.. now asap” - Rathlavath Ganesh (18/03/26, 1 Star)

“bro don’t use this app this is the worst app iam ever seen . From the amount allotted they just give 60 percent of amount for 7 days only . Iam taken a loan of amount 1500 but from that just I get 900 but now It showing to pay 1500” - ravinder solanki (18/03/26, 3 Star)

Users ne likha hai ki repayment ke liye help maangi thi lekin koi response nahi mila.

Yeh reviews sirf tip of the iceberg hain. Reddit aur YouTube par bhi bahut se users ne same experience share kiya hai – partial disbursement, 7 din ka trap, aur agar time par nahi bhara toh contacts mein messages aur calls se harassment. Ek user ne bataya ki app gallery aur contacts access maangta hai taaki non-payment par blackmail kar sake. Positive reviews zyadatar fake lagte hain kyunki negative reviews mein users khud bol rahe hain “positive reviews are also Fake”.

Kyun Yeh 7 Day Loan App Itna Dangerous Hai?

Pehle toh heavy charges ki baat. Aap ₹900 lete ho, ₹1,500 wapas karte ho 7 din mein – yeh koi normal loan nahi, yeh trap hai. Agar aap miss kar gaye toh daily penalty lagti hai aur amount badhta jaata hai. Dusra bada issue data privacy ka hai. App gallery, contacts, SMS, location sab access maangta hai. Users ke according non-payment par yeh photos edit karke nude bana dete hain aur family-friends ko bhej dete hain. Yeh India mein bahut common scam tactic hai aur 2026 mein government ne 87+ illegal loan apps block kiye hain.

Teesra, customer support almost non-existent hai. Number diya hota hai lekin call nahi lagta. Email bhejte ho toh reply nahi aata. Isliye users ko lagta hai ki yeh sirf paisa nikaalne ka tool hai.

GaneshFast Loan App Real or Fake? Expert Analysis

Agar hum sab reviews ko dekhen toh yeh GaneshFast Loan App Scam category mein aata hai. Official claims (long tenure, low interest) aur real user experience (7 days, heavy charges, blackmail) mein bada gap hai. RBI registered NBFC nahi dikh raha aur developer details bhi suspicious hain. YouTube par bhi bahut se videos hain jismein is app ko “real or fake” bolke expose kiya gaya hai.

Aise apps ka pattern same hota hai:

- Chhota loan approve karo

- Kam paisa do

- Short tenure rakho

- Agar nahi bhara toh harassment shuru

Isliye hum recommend karte hain – GaneshFast Personal Loan App se door raho. Agar aapko chhota loan chahiye toh family se maango, ya RBI approved apps jaise MoneyTap, EarlySalary, Bajaj Finserv use karo jo regulated hain.

GaneshFast Personal Loan App Ke Pros Aur Cons

Pros (sirf official claim ke hisaab se):

- Instant approval (lekin sirf paper par)

- No collateral

- Play Store par available

Cons (real users ke hisaab se):

- Approved amount se sirf 60% milta hai

- 7 din mein full repayment + heavy service fee

- Blackmail aur photo morphing ki dhamki

- Support nahi milta

- Positive reviews fake

- High effective interest rate

FAQ – GaneshFast Personal Loan App Ke Bare Mein Common Sawal

Q1. GaneshFast Personal Loan App real hai ya fake?

A: Reviews ke hisaab se yeh fake fraud practices wala app hai. 7 day loan trap mein fas jaate ho.

Q2. Isme kitna interest lagta hai?

A: Official 15% APR dikhata hai lekin asal mein service fee ke saath 3000%+ effective rate ban jaata hai ek saal ke hisaab se.

Q3. Loan kitne din ka hota hai?

A: Mostly 7 days. Official description mein 91-360 din likha hai lekin users ko 7 din hi mil raha hai.

Q4. Kya photo blackmail hota hai?

A: Haan, multiple reviews mein users ne yeh complaint kiya hai ki non-payment par edited nude photos contacts mein bheje jaate hain.

Q5. App uninstall karne ke baad bhi problem hoti hai?

A: Agar aapne already loan liya hai toh repayment pressure rehta hai. Uninstall karne se pehle screenshot le lo sab ka.

Q6. Positive reviews kyun hain?

A: Users bol rahe hain ki woh fake hain ya paid hain.

Q7. Kya yeh RBI approved hai?

A: Koi clear proof nahi mila. RBI ne aise unregulated apps ke against warning diya hai.

Q8. Loan apply karne se pehle kya check karein?

A: Sirf Play Store reviews padho, rating mat dekho. Negative reviews zyada matter karte hain.

Aur bhi questions ho toh comment karo.

Agar Aapke Saath Fraud Hua Hai Toh Complaint Kaise Karein? Step-by-Step Process (2026 Updated)

Agar aapne GaneshFast se loan liya aur ab lag raha hai fraud hua hai (kam paisa mila, heavy charges, blackmail), toh turant action lo. Paise recover hone ke chances hain agar jaldi report karoge.

- Sab evidence collect karo

- Loan approval screenshot

- Disbursed amount (₹900) ka bank statement

- Repayment demand messages

- Threat messages (nude photo wali)

- App ke screenshots

- Google Play Store par report karo

App open karo → More → Report → “It’s a scam or fraud” select karo aur details likho. 1-star review daalo with screenshots. - National Cyber Crime Reporting Portal par complaint

Website: https://cybercrime.gov.in

Ya helpline number 1930 dial karo (24×7 free).

Category select karo “Financial Fraud” → “Online Cheating” ya “Illegal Loan App”.

FIR automatically register ho jaati hai aur cyber cell investigate karta hai. - Local Police Station / Cyber Cell mein FIR

Nearest police station jaao ya cyber crime cell mein. IPC Section 420 (cheating) aur 503 (criminal intimidation) ke under case darj karwao. - RBI / Sachet Portal par bhi report

https://sachet.rbi.org.in par jaake complaint daalo. Yeh banks aur NBFC ke against helpful hai. - Bank se dispute karo

Agar UPI ya bank account se transaction hua hai toh bank customer care ko call karo aur chargeback maango. - Consumer Helpline

14448 par call karo ya consumerhelpline.gov.in par complaint.

Jitni jaldi report karoge, utna better. Government 2026 mein loan app scams par strict hai aur kai cases mein paise wapas bhi hue hain.

Conclusion: GaneshFast Se Door Raho, Safe Loan Options Choose Karo

GaneshFast Personal Loan App ek typical 7 day loan app hai jo heavy charges ke saath users ko trap karta hai. Play Store ke critical reviews (Dharmendra Kumar, Patrick Star, Gyalzen Sherpa wagairah) sab yahi bol rahe hain – fraud, partial disbursement, blackmail. Official description mat mano, reviews par bharosa karo.

Agar aapko sach mein loan chahiye toh banks jaise SBI, HDFC, ya RBI registered apps use karo. Family se maango, ya salary advance schemes dekho. Ek galat app download karne se aapki privacy, mental peace aur paisa sab chala ja sakta hai.

Is article ko share karo taaki aur log bach sakein. Koi experience ho toh comment mein batao. Safe rahiye, smart borrow kijiye!

(Word count: 1480+)

Keywords: GaneshFast Personal Loan App Review 2026, GaneshFast Loan App Scam, 7 Day Loan App Fraud, GaneshFast Real or Fake, heavy charges loan app India.

Agar aapko koi change chahiye toh bataiye!