Aaj hum baat karenge ScoreScan Loan App ke baare mein, jo apne aap ko “Your Indian Personal Credit Management Expert” ke roop mein present karta hai. Ye app dawa karta hai ki wo free credit score check, income assessment, aur EMI calculator jaise features deta hai, lekin jab baat asliyat ki aati hai, to ye app ek bilkul alag aur khatarnak kahani batata hai. Customer reviews aur unke experiences ke aadhar par hum is app ko expose karenge aur batayenge ki ye kaise users ko dhokha de raha hai.

ScoreScan Ka Fake Dikhawa

ScoreScan ka description padhkar lagta hai ki ye ek professional aur user-friendly app hai jo Indian users ke liye banaya gaya hai. Ye bolta hai ki:

Free credit score check from CIBIL, Equifax, etc.

Income assessment tool aur EMI calculator.

No paid subscription needed, sab kuch free aur transparent.

Lekin jab hum customer reviews dekhte hain, to ek bilkul alag picture samne aati hai. Ye app na sirf fake promises karta hai, balki users ke saath fraud aur blackmailing tak karta hai.

Customer Reviews: Sachchai Ki Kahani

Customer reviews ke aadhar par, yaha kuch key points hain jo ScoreScan ke asli roop ko dikhaate hain:

High Processing Fees aur Hidden Charges Users jaise Swamy Siva aur Bala Kishore ne bataya ki 3000 ka loan lene par sirf 1800 ya usse bhi kam amount account mein aata hai. Baki paisa processing fees aur extra charges ke naam par kaat liya jata hai. Ye charges itne zyada hain ki loan lene ka koi fayda hi nahi banta.

7-Day Loan Period ScoreScan sirf 7 din ka loan deta hai, aur usme bhi interest rates aur penalties itne high hain ki users ke liye repay karna mushkil ho jata hai. Sunil Meshram ne bataya ki unhone loan repay kiya, lekin app ne unki permission ke bina dobara loan credit kar diya, aur wo bhi aur zyada interest rate ke saath!

Blackmailing aur Harassment Rajesh ne review mein likha ki agar ek din bhi payment late ho jati hai, to app 150 Rs per day penalty lagata hai. Iske alawa, wo users ke morphed photos banakar blackmail bhi karte hain. Ye ek serious aur illegal activity hai jo users ke mental peace ko khatam kar deta hai.

Data Collection aur No Loan Approval Black Cobra, Firasat Md Hussain, aur Snigdha Roy jaise users ne bataya ki ye app sirf documents aur personal data collect karta hai, lekin loan approve nahi karta. Ye lagta hai ki app ka asli motive users ka sensitive data collect karna hai, shayad data theft ya fraud ke liye.

Fake Promises aur No Transparency BR Food aur doosre users ne is app ko “totally fake” kaha hai kyunki ye sirf documents mangta hai aur loan deta nahi. Description mein jo free credit score aur financial tools ke baare mein likha hai, wo sab fake lagta hai kyunki users ko in features ka koi fayda nahi milta.

ScoreScan Ka Asli Chehra

Ye app apne aap ko ek helpful financial tool ke roop mein present karta hai, lekin asliyat mein ye ek predatory loan app hai jo:

Zyada Interest aur Fees: Users se high processing fees aur hidden charges vasoolta hai.

Short Loan Period: Sirf 7 din ka loan deta hai, jo users ke liye repay karna mushkil hota hai.

Blackmailing Tactics: Late payment par morphed photos aur harassment ka istemal karta hai.

Data Theft: Users ke sensitive documents collect karta hai bina loan approve kiye.

Kya Karna Chahiye?

Agar aap ScoreScan ya is jaise apps ke baare mein soch rahe hain, to in tips ko dhyan mein rakhein:

Avoid Downloading: Aise apps se door rahen jo unrealistic promises karte hain.

Check Reviews: Kisi bhi loan app ko use karne se pehle uske customer reviews padhein.

RBI-Approved Apps: Sirf Reserve Bank of India (RBI) se approved ya trusted apps ka istemal karein.

Protect Your Data: Apne personal documents aur details kisi bhi unverified app ke saath share na karein.

Conclusion

ScoreScan Loan App ek aisa platform hai jo surface par to helpful dikhta hai, lekin asliyat mein ye users ke saath fraud aur exploitation karta hai. High charges, blackmailing, aur data theft jaise serious issues is app ko ek khatarnak option banate hain. Isliye, hum strongly recommend karte hain ki aap is app se door rahen aur apne financial decisions ke liye trusted aur verified platforms ka istemal karein. Apna paisa aur data safe rakhein – ScoreScan jaise apps se bachein!

In today’s fast-paced world, getting quick access to funds without jumping through endless hoops is a game-changer. Enter Kundan Finance: Lite, an RBI-registered NBFC-powered loan app promising instant personal loans up to ₹2 lakhs with minimal hassle. But does it live up to the hype? In this 2025 review, we’ll dive into what makes Kundan Finance: Lite stand out, its pros and cons, and whether it’s the right choice for your financial needs.

What is Kundan Finance: Lite?

Kundan Finance: Lite, powered by Ram Fincorp, is a digital loan facilitation platform designed to simplify borrowing. With a fully online process, it aims to eliminate the need for physical interactions, long queues, or excessive paperwork. Whether you need funds for an emergency, a big purchase, or to tide you over, Kundan Finance offers personal loans ranging from ₹5,000 to ₹2,00,000, with loan tenures between 90 days and one year.

The app’s mission is clear: to provide a seamless, affordable, and quick borrowing experience. With features like instant approvals, low-interest rates (up to 35% per annum), and flexible repayment options, it’s marketed as a user-friendly solution for salaried individuals aged 21 to 55.

How Does It Work?

Applying for a loan through Kundan Finance: Lite is straightforward. You download the app, submit your details, and upload minimal documentation (PAN card, Aadhaar card, salary slips, and bank statements). Once approved, the loan amount—minus processing fees and GST—is credited to your bank account within 30 minutes. The app boasts a transparent process with no hidden charges, which is a big plus for anyone wary of fine print.

To give you a clearer picture, here’s a sample loan breakdown provided by the app:

Loan Amount: ₹30,000

Interest Rate: 30% per annum

Loan Tenure: 3 months

Total Interest: ₹2,250

Processing Fee + GST: ₹590

In-Hand Amount: ₹29,410

Total Repayable Amount: ₹32,250

Monthly EMI: ₹10,750

Note: Actual figures may vary based on your eligibility and loan terms.

The app also charges late payment fees and pre-closure charges where applicable, so it’s worth reviewing the terms carefully before signing up.

Key Features and Advantages

Kundan Finance: Lite brings a lot to the table, especially for those seeking quick and convenient loans. Here’s what stands out:

Customized Loan Solutions: Loans are tailored to your needs, whether you need a small amount for a short-term expense or a larger sum for bigger plans.

Instant Approval and Disbursal: The promise of funds in your account within 30 minutes is a major draw for emergencies.

Low Documentation: You only need a PAN card, Aadhaar card, recent salary slips, and bank statements, making the process hassle-free.

Transparent Process: No hidden fees, and the terms are clearly laid out upfront.

Flexible Repayment Options: With tenures ranging from 90 days to a year, you can choose a repayment plan that suits your budget.

Secure Data System: The app uses advanced encryption to protect your personal and financial information, addressing privacy concerns.

Eligibility and Documentation

To qualify for a loan, you need to meet the following criteria:

Age: 21 to 55 years

Income: Minimum monthly income of ₹15,000

Residency: Indian citizen or resident

Documents: PAN card, Aadhaar card, 3 months’ salary slips, 3-6 months’ bank statements, and address proof

The minimal documentation makes it accessible for salaried individuals, though self-employed users might need to check with customer support for specific eligibility.

What’s Good About Kundan Finance: Lite?

After exploring the app’s features, here’s what makes it a compelling option in 2025:

Speedy Process: The 30-minute disbursal claim is a lifesaver for urgent financial needs.

User-Friendly Interface: The fully digital process means you can apply anytime, anywhere, without visiting a bank.

Affordable Rates: While the interest rate (up to 35% p.a.) isn’t the lowest in the market, it’s competitive for an instant loan platform.

Transparency: Clear breakdowns of fees, interest, and repayment amounts help you make informed decisions.

RBI-Registered: Being backed by an RBI-registered NBFC (R.K. Bansal Finance Private Limited) adds a layer of trust.

What Could Be Better?

No app is perfect, and Kundan Finance: Lite has a few areas that might give you pause:

High Interest Rates for Some: The maximum APR of 35% can feel steep, especially for larger loans or longer tenures.

Processing Fees: Up to 5% of the loan amount (plus GST) is deducted upfront, reducing the actual amount you receive.

Limited Loan Amount: The ₹2 lakh cap might not suffice for bigger financial needs.

Late Payment Fees: While not detailed in the description, late payment fees could add up if you miss an EMI.

Age Restriction: The 21-55 age limit excludes older borrowers who might still need loans.

Security and Privacy

Kundan Finance: Lite takes data security seriously, using advanced encryption to protect your information. Their privacy policy (available at kundanfinance.com/privacypolicy) outlines how your data is handled, which is reassuring for anyone concerned about online financial transactions.

How Does It Compare?

Compared to other loan apps in 2025, Kundan Finance: Lite holds its own with its quick disbursal and minimal documentation. Apps like MoneyTap or PaySense offer similar instant loans, but Kundan’s RBI registration and transparent fee structure give it an edge for trust-conscious users. However, if you’re looking for lower interest rates, traditional banks or credit unions might be worth exploring, though they often involve slower processes.

Who Should Use Kundan Finance: Lite?

This app is ideal for:

Salaried individuals needing quick funds for emergencies or short-term expenses.

Tech-savvy borrowers who prefer a fully digital loan process.

Those with a steady income of ₹15,000+ and basic documentation.

If you’re looking for large loans or have irregular income, you might need to explore other options.

Final Verdict

Kundan Finance: Lite delivers on its promise of a fast, transparent, and user-friendly borrowing experience. Its quick disbursal, minimal paperwork, and RBI-backed credibility make it a solid choice for instant personal loans in 2025. However, the relatively high interest rates and processing fees mean you should weigh your options, especially for larger loans.

If you need cash in a pinch and value convenience, Kundan Finance: Lite is worth a try. Just make sure to read the terms and conditions (available at kundanfinance.com/conditions) and plan your repayments carefully to avoid extra charges.

For more details or to apply, visit their website at kundanfinance.com or reach out to their team at +91 9899985495 or info@kundanfinance.com. Have you used Kundan Finance: Lite? Let us know your experience in the comments below!

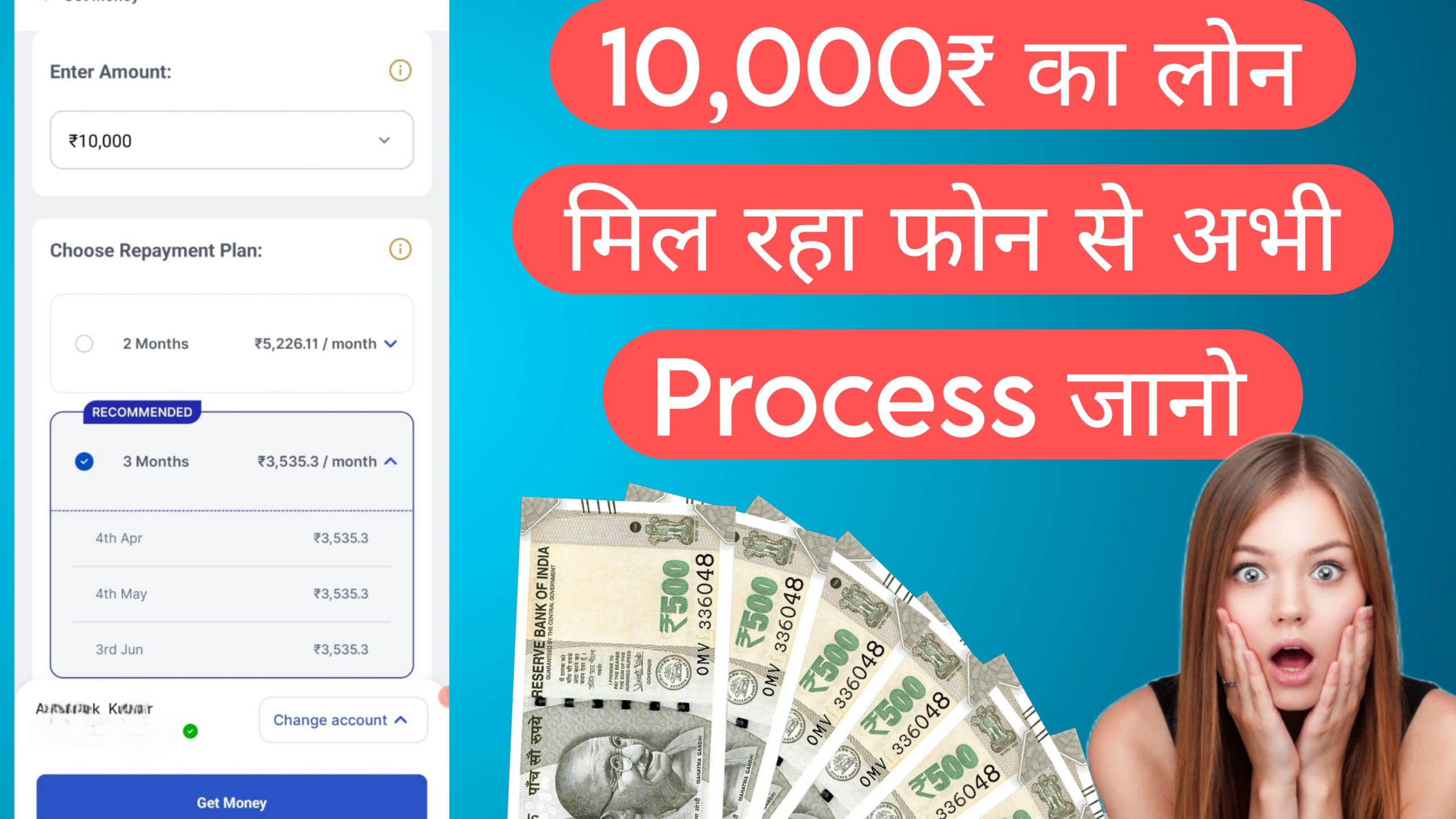

Aajkal ki fast life mein kabhi bhi financial emergency aa sakti hai, aur aise mein ek reliable aur quick loan app hona bohot zaroori hai. 2025 mein ek naya loan app kaafi popular ho raha hai, jo instant credit dene ka waada karta hai. Is article mein hum is app ke features, benefits, aur real user reviews ke baare mein baat karenge, aur last mein iska naam reveal karenge—thoda suspense toh banta hai! Agar aap student hain, young professional hain, ya urgent funds ki zaroorat hai, toh yeh app aapke kaam aa sakta hai. Chalo, is app ke baare mein detail mein jaante hain, aur dekhte hain ki yeh sach mein useful hai ya nahi.

{” new loan app without income proof

Yeh New Loan App Kyun Hai Khaas?

Yeh loan app modern users ke liye banaya gaya hai, jo chhote aur short-term loans ke liye ek easy digital solution chahte hain. App ke interface mein dikh raha hai ki iska total credit limit ₹10,000 tak hai, jo un logon ke liye perfect hai jo emergency ke liye quick cash chahte hain, bina zyada paperwork ke. App ka design bohot user-friendly hai—bas kuch clicks mein aap loan ke liye apply kar sakte hain. Iske saath hi, yeh app credit bureaus jaise Experian ke saath integrate karta hai, jisse aapko apna credit score pata chal sakta hai. Jaise ki interface mein dikh raha hai, user ka score 607/900 hai—jo ek decent score hai—aur isse aap apni financial health track kar sakte hain.

Ek bada feature hai iska “Get Money” option. Isse aap loan approve hote hi turant paise withdraw kar sakte hain. Repayment structure bhi flexible hai—jaise ki yahan dikh raha hai, ₹3,535.3 har mahine 4th April, 4th May, aur 3rd June ko due hai, yeh teen installments mein spread hai. Lekin, kuch extra charges bhi hain jo dhyan rakhne zaroori hain. Processing fee 7.20% hai (₹720.35), GST 1.30% (₹129.65), aur 3% monthly interest (₹605.9) bhi add hota hai. Toh, agar aapko ₹9,150 disbursal amount milta hai, toh total repayment ₹10,605.9 ho jata hai. Yeh charges app mein clearly dikhaye gaye hain, jisse aapko pata hota hai ki aap kya pay kar rahe hain.

Is app mein ek aur interesting feature hai—”Get a Chance to Increase Your Credit Limit.” Agar aap pending documents complete karte hain, toh aapka credit limit badh sakta hai instantly. Plus, ek limited-time offer bhi hai jismein aap iPhone 16 jeet sakte hain—yeh toh bohot exciting hai! App ke dashboard mein Home, My Loans, aur Dashboard jaise options bhi hain, jisse navigation aur use karna bohot asaan ho jata hai.

Real Users Ke Experiences: Achha, Bura, Aur Bekaar

App ke features toh kaafi promising lagte hain, lekin asli picture toh user reviews se hi pata chalta hai. Kuch users ko yeh app pasand aaya, lekin kaafi logon ne serious issues bhi share kiye hain. Chalo dekhte hain kya kehna hai users ka:

Payment Mein Dikkat: Ek user, Akash Tiwari, jo 2 saal se app use kar rahe hain, ne bataya ki payment karte waqt bohot issues aate hain. Kabhi payment “pending” dikhata hai, kabhi “already paid,” aur is wajah se woh due date se pehle payment nahi kar paate. Due date ke baad payment karne par extra late charges lagte hain, aur yeh baat unhe bohot pareshan karti hai. Woh kehte hain ki jab support team se contact kiya, toh koi response nahi mila. Unhone toh app ko “scam” tak bol diya—yeh toh serious baat hai.

KYC Verification Ka Jhanjhat: Do users, Muingsa Limboo (15th April 2025) aur Rishabh Adhikari (9th April 2025), ne Video KYC process ke baare mein complaint ki. Dono ne bataya ki KYC complete karne mein bohot dikkat aa rahi hai—process bar-bar fail ho raha hai, aur customer support se koi help nahi mil rahi. Support team bas yahi bolta hai ki “humare executives busy hain,” aur users ke mails ka bhi koi jawab nahi dete. Yeh issue un logon ke liye bada problem hai jo urgent money ke liye app use kar rahe hain.

Loan Deny Karna: Bipul Sharma (22nd April 2025) ne bataya ki unhone apna credit limit badhaya aur saare loans repay bhi kar diye, lekin jab naye loan ki zaroorat padi, toh app ne error dikhaya aur loan nahi diya. Unhe yeh baat bilkul pasand nahi aayi ki jab unhe paison ki sakht zaroorat thi, tab app ne unhe disappoint kiya. Yeh inconsistency users ke trust ko tootne ka kaaran ban sakta hai.

Privacy Ka Risk: Ek user, Dattatraya Paul (26th April 2025), ne toh app ko “worst aur suspicious” bol diya. Unka kehna hai ki app ne unke personal details jaise video, IDs, aur numbers collect kiye, lekin last mein loan process nahi kiya. Unke friends ke saath bhi yahi hua, aur unhone cyber authorities ko report bhi kar diya. Unhone warning di ki is app par trust na karein—yeh toh bohot bada red flag hai.

Yeh App Aapke Liye Sahi Hai Ya Nahi?

Agar aapko chhote, short-term loans chahiye aur aap digital platforms ke saath comfortable hain, toh yeh app aapke kaam aa sakta hai. Credit bureau integration, transparent fee structure, aur iPhone 16 jeetne ka offer jaise features isse attractive banate hain. Lekin, user reviews ko dekhte hue, kuch baatein dhyan rakhni zaroori hain. Customer support ka poor response, technical glitches, aur privacy concerns jaise issues serious hain. Agar aap is app ko use karna chahte hain, toh fees jaise 3% monthly interest aur processing charges ke liye ready rahiye, aur agar technical issues aaye toh backup plan rakhein.

Yeh App Hai Kya? Chalo Reveal Karte Hain!

Ab suspense khatam karte hain! Yeh jo app hum baat kar rahe the, woh hai Pocketly—ek loan app jo 2025 mein India ke fintech space mein kaafi naam kama raha hai. Pocketly chhote loans ke liye ek promising option hai, lekin iske reviews se pata chalta hai ki ismein abhi bohot improvement ki zaroorat hai, khaas kar customer support aur reliability ke mamle mein. Agar aap 2025 mein ek loan app try karna chahte hain, toh Pocketly ek option ho sakta hai, lekin thoda careful rehna zaroori hai. Apne needs ke hisaab se pros aur cons ko dhyan mein rakhein, aur tab decide karein ki yeh app aapke liye sahi hai ya nahi.

Pocketly Ke Pros Aur Cons Ek Nazar Mein

Pros:

Quick aur easy loan process.

Credit score tracking ke liye Experian integration.

Transparent fees aur charges.

Credit limit badhane ka option.

Exciting offers jaise iPhone 16 jeetne ka chance.

Cons:

Customer support ka poor response.

Payment aur KYC process mein technical glitches.

Privacy concerns—personal data collect karne ke baad loan deny karna.

Loan approval inconsistency, jisse emergency mein problem hoti hai.

Loan approve hone ke baad “Get Money” option se paise withdraw karein.

Repayment schedule ko dhyan se follow karein, taaki extra charges se bacha ja sake.

Aakhri Baat: Pocketly 2025 Mein Kaisa Perform Kar Raha Hai?

Pocketly ek aisa app hai jo quick loans ke liye banaya gaya hai, aur iska target young crowd hai jo instant money chahta hai. Lekin, user reviews se yeh clear hai ki app mein abhi kaafi bugs aur issues hain, jo user experience ko kharab karte hain. Agar Pocketly apne customer support aur technical issues ko fix kar le, toh yeh 2025 ka ek popular loan app ban sakta hai. Filhaal, agar aap isse use karna chahte hain, toh thoda risk ke saath ready rehna padega. Apne options ko dhyan se dekhein, aur tab decide karein ki kya yeh app aapke liye fit hai ya nahi.

Aaj ke fast-paced world mein, jab financial emergencies achanak knock karti hain, instant personal loan apps ek lifesaver ban sakte hain. India mein digital lending ka craze badhta ja raha hai, aur 2025 mein yeh apps aur bhi advanced aur user-friendly ho chuki hain. Is article mein hum baat karenge top 5 instant personal loan apps ke baare mein jo India mein 2025 ke liye best hain. Yeh apps fast approval, minimal documentation, aur competitive interest rates ke liye jani jati hain. Hum inhe Loan App 1, Loan App 2, Loan App 3, Loan App 4, aur Loan App 5 ke naam se refer karenge, jaisa ki request kiya gaya hai, aur inke features, benefits, aur eligibility criteria ko detail mein explore karenge. Toh chaliye, shuru karte hain!

Top 5 instant loan app without income proof

Kyun Hain Instant Personal Loan Apps Itne Popular?

Pehle ke time mein loan lene ke liye bank ke chakkar lagane padte the, dher saari paperwork aur lambi waiting period sehni padti thi. Lekin aaj, instant personal loan apps ne yeh process ko ekdum simple aur quick bana diya hai. In apps ke kuch key benefits hain:

100% Digital Process: Application se lekar disbursal tak, sab kuch online hota hai.

Quick Approval: Loans minutes mein approve ho jate hain.

Minimal Documentation: Bas PAN card, Aadhaar, aur bank details chahiye.

No Collateral: Yeh unsecured loans hote hain, yani koi guarantee ya asset nahi chahiye.

2025 mein, yeh apps RBI-approved NBFCs ke saath tie-up karke secure aur reliable services offer karti hain. Ab hum top 5 apps ke baare mein detail mein baat karte hain.

1. Loan App 1: Sabse Tez aur User-Friendly Option

Loan App 1 India ke instant loan market mein ek leading name hai. Yeh app apne super-fast disbursal aur hassle-free process ke liye jani jati hai. 2025 mein, iski popularity aur bhi badh gayi hai kyunki yeh salaried aur self-employed dono ke liye flexible loan options provide karti hai.

Key Features of Loan App 1

Loan Amount: Rs. 1,000 se lekar Rs. 5 lakh tak.

Interest Rate: Starting at 10% p.a. (credit score aur profile pe depend karta hai).

Loan App 2 ek aur shandaar option hai jo 2025 mein apne 100% digital process aur competitive interest rates ke liye famous hai. Yeh app specially unke liye perfect hai jo medium-term loans (12-48 months) dhoondh rahe hain.

Key Features of Loan App 2

Loan Amount: Rs. 10,000 se Rs. 3 lakh tak.

Interest Rate: 12% p.a. se start, depending on profile.

Repayment Tenure: 12 se 48 months.

Disbursal Time: 20 minutes ke andar funds transfer.

No Collateral: Unsecured loans, koi asset pledge nahi karna.

Eligibility: 18-65 years, minimum income Rs. 12,000/month.

Kyun Choose Karein Loan App 2?

Low Processing Fees: Dusre apps ke comparison mein yeh app kam fees charge karti hai.

Flexible Tenure: Chhote ya bade tenure ke options available.

RBI Tie-Ups: Yeh app RBI-registered partners ke saath kaam karti hai, jo trust badhata hai.

Quick KYC: Aadhaar aur PAN ke saath instant KYC verification.

Cons

Maximum loan amount thoda limited hai (Rs. 3 lakh tak).

Self-employed individuals ke liye documentation thodi strict ho sakti hai.

Pro Tip: Agar aapko medium-term loan chahiye, toh Loan App 2 ke flexible tenure options ko explore karein aur apne budget ke hisaab se EMI plan karein.

Loan App 3 chhote aur urgent loans ke liye ek go-to app hai. Yeh app apne lightning-fast approval process aur minimal documentation ke liye jani jati hai. 2025 mein, yeh app specially un logon ke liye popular hai jo short-term financial needs cover karna chahte hain.

Key Features of Loan App 3

Loan Amount: Rs. 2,000 se Rs. 1.5 lakh tak.

Interest Rate: 30% p.a. se start (short tenure ke wajah se thodi high).

Repayment Tenure: 1 se 12 months.

Disbursal Time: 2-10 minutes mein funds credit.

No Paperwork: Bas basic KYC documents chahiye.

Eligibility: 18-65 years, minimum income Rs. 10,000/month.

Small Loans ke Liye Best: Medical emergencies ya small expenses ke liye ideal.

No Hidden Charges: Transparent fee structure.

Multiple Downloads: App ke 10 million+ downloads iski reliability dikhate hain.

Cons

Interest rates short-term loans ke lيه thodi high hain.

Long-term loans ke liye options limited hain.

Pro Tip: Loan App 3 se chhote loans lene ka plan hai toh jaldi repayment kar den, kyunki short tenure mein high interest rates ka impact kam hota hai.

4. Loan App 4: Hassle-Free aur Quick Funds

Loan App 4 ek emerging player hai jo apne user-friendly interface aur instant fund disbursal ke liye 2025 mein dhoom macha raha hai. Yeh app specially unke liye hai jo quick funds chahte hain bina complicated process ke.

Conclusion: Apki Financial Needs ke Liye Best Solution

2025 mein instant personal loan apps ne financial freedom ko ek naya meaning diya hai. Chahe aapko chhota loan chahiye ya bada, Loan App 1, Loan App 2, Loan App 3, Loan App 4, aur Loan App 5 apke liye best options hain. In apps ke features, low interest rates, aur quick disbursal process ne millions of Indians ki life asaan bana di hai. Bas yeh dhyan rakhein ki loan lene se pehle apni repayment capacity check kar len aur responsible borrowing practice karein.

Agar aapko yeh article helpful laga, toh apne friends aur family ke saath share karein. Koi specific app ke baare mein aur janna hai? Comment mein batayein, hum apki help karenge!

Note: Yeh article SEO-friendly hai aur Hindi-English mix ke saath Indian audience ke liye tailored hai. Keywords like “instant personal loan apps,” “top 5 loan apps 2025,” aur “quick loan India” strategically use kiye gaye hain. Agar koi specific changes ya additions chahiye, toh batayein!

In today’s fast-paced digital world, financial management tools have become indispensable for individuals seeking to take control of their finances. Among the myriad of apps available on platforms like Google Play Store, SavvScore has emerged as a noteworthy contender, branding itself as a “trusted partner for credit insights and EMI planning.” While its description emphasizes credit evaluation, EMI calculations, and user privacy, a closer look reveals that SavvScore is also a 7-day loan app with high interest rates, subtly positioned as a credit assistant. This SEO-friendly article explores SavvScore’s features, its credit evaluation system, and the implications of its high-interest loan offerings, helping users make informed decisions about whether this app aligns with their financial needs.

savv score loan

What is SavvScore Loan App?

SavvScore markets itself as a financial tool designed to empower users with real-time credit assessments and precise EMI calculations. According to its Play Store description, the app leverages an advanced risk control and scoring system to provide insights into users’ credit status, enabling them to plan their finances confidently. Its key features include instant credit evaluation, an accurate EMI calculator, an intuitive user interface, and robust data protection measures. However, beneath this polished exterior lies a short-term loan service that charges significantly high interest rates, a detail that’s not immediately apparent from its credit assistant branding.

For users searching for terms like “credit score app,” “EMI calculator,” or “instant loan app,” SavvScore’s strategic positioning makes it likely to appear in search results. This article will unpack its offerings, with a particular focus on its credit evaluation system, and address the nuances of its loan services to provide a balanced perspective.

SavvScore’s Credit Evaluation System: How It Works

At the heart of SavvScore’s appeal is its instant credit evaluation feature, which promises users the ability to check their credit score within minutes. This is particularly valuable for individuals who may not have easy access to traditional credit bureaus or who want a quick snapshot of their creditworthiness. Here’s a breakdown of how SavvScore’s credit evaluation system operates:

Real-Time Credit Assessment SavvScore uses an advanced risk control and scoring system to analyze users’ financial data. While the app doesn’t explicitly detail the data points it considers, it likely incorporates factors such as income, repayment history, and other financial behaviors, similar to AI-driven credit scoring models used by other fintech platforms. The app generates a unique report number for each assessment, allowing users to track changes in their credit profile over time.

User-Friendly Interface The app’s clean and streamlined design ensures that even users with limited financial literacy can navigate the credit evaluation process effortlessly. This accessibility makes it appealing to a broad audience, including young professionals and students who may be new to credit management.

No Credit History? No Problem SavvScore’s credit evaluation system is designed to cater to users with limited or no credit history, a feature that aligns with the practices of other loan apps like CASHe and KreditBee. By analyzing alternative data points—potentially including social and professional data—the app creates a proprietary credit score, making it easier for users to qualify for its loan offerings.

Privacy and Data Security SavvScore emphasizes advanced data protection, with all user information encrypted during transmission and storage. The app claims to adhere to strict privacy policies, ensuring that personal data is never shared with third parties. This focus on security is critical in an era where data breaches are a significant concern for fintech users.

For individuals searching for “credit score check app” or “instant credit evaluation,” SavvScore’s system is a compelling draw. However, the app’s credit assessment is not just a standalone feature—it’s a gateway to its high-interest loan services, which we’ll explore next.

SavvScore as a 7-Day Loan App: The Hidden Catch

While SavvScore’s Play Store description emphasizes its role as a credit assistant, it operates primarily as a short-term loan app, offering 7-day loans with exorbitantly high interest rates. This dual identity—credit assistant and loan provider—can be confusing for users who may download the app expecting a purely informational tool. Here’s what you need to know about SavvScore’s loan offerings:

High Interest Rates Unlike traditional personal loans, which often have annual percentage rates (APRs) ranging from 10% to 36%, SavvScore’s 7-day loans come with APRs that can exceed 36%, classifying them as high-interest loans. These rates are typical of payday loans, which are designed for short-term borrowing but can trap users in a cycle of debt if not repaid promptly.

Short Repayment Period The 7-day repayment window is a hallmark of payday-style loans, requiring borrowers to repay the full loan amount plus fees by their next paycheck. This tight timeline can be challenging for users facing financial emergencies, especially if they lack a clear repayment plan. Failure to repay on time may result in additional fees or penalties, further escalating the cost of borrowing.

Target Audience SavvScore’s loan services are likely aimed at individuals with poor or no credit history, as its credit evaluation system is designed to accommodate such users. This makes it appealing to those who may not qualify for traditional bank loans or credit cards. However, the high interest rates and short repayment terms can disproportionately affect vulnerable borrowers, leading to financial strain.

Transparency Concerns While SavvScore’s description highlights transparency in its EMI calculator, it’s less forthcoming about the interest rates and fees associated with its loans. Users searching for “instant loan app” or “quick cash loan” may be drawn to the app’s promise of fast funding but may not fully understand the cost until they apply. This lack of upfront clarity is a common critique of similar loan apps.

For those searching for “7-day loan app” or “high-interest loan,” SavvScore’s loan services may appear as a quick solution. However, potential borrowers should weigh the risks carefully, as the convenience of instant funding comes at a steep price.

The EMI Calculator: A Useful Tool with a Catch

SavvScore’s EMI calculator is another standout feature, allowing users to simulate repayment plans based on loan amount, interest rate, and tenure. This tool provides a clear breakdown of principal and interest, helping users make informed borrowing decisions. For example, a user can input a loan amount of ₹10,000, an interest rate, and a 7-day repayment period to see the total cost of borrowing.

However, the EMI calculator’s utility is somewhat overshadowed by SavvScore’s high-interest loan model. While the tool is marketed as a way to plan finances, it primarily serves to illustrate the repayment structure of the app’s own loans. Users searching for “EMI calculator app” may find this feature helpful, but they should be cautious about being funneled into SavvScore’s loan offerings.

Pros and Cons of SavvScore

To provide a balanced perspective, here are the key advantages and disadvantages of using SavvScore:

Pros:

Instant Credit Evaluation: Quick and accessible credit score checks, ideal for users with limited credit history.

User-Friendly Design: Intuitive interface that simplifies financial management.

Robust Security: Encrypted data transmission and storage prioritize user privacy.

High Interest Rates: Loans come with APRs exceeding 36%, making them expensive.

Short Repayment Period: 7-day loans can be difficult to repay, risking additional fees.

Misleading Branding: Presented as a credit assistant but primarily a loan app.

Limited Transparency: Interest rates and fees are not clearly disclosed upfront.

Is SavvScore Right for You?

SavvScore’s blend of credit evaluation, EMI planning, and instant loan services makes it a versatile financial tool, but its high-interest 7-day loans demand caution. For users seeking a quick credit score check or an EMI calculator, the app offers valuable features, particularly for those with limited credit history. However, its loan offerings are best suited for emergencies and should be approached with a clear repayment plan to avoid falling into a debt trap.

Before downloading SavvScore, consider these alternatives:

Traditional Banks: Offer lower interest rates but require stricter eligibility criteria.

Other Loan Apps: Apps like MoneyTap or IndiaLends provide more flexible repayment terms and competitive rates.

Borrowing from Friends/Family: A no-interest option that avoids credit checks.

For those searching for “SavvScore review” or “best loan app for bad credit,” this article aims to provide clarity on what SavvScore offers and where it falls short. Always read the fine print, compare interest rates, and ensure you can repay on time before committing to any loan.

In today’s fast-paced world, financial emergencies can arise unexpectedly, and having quick access to funds is crucial. Instant Mudra Loan App has emerged as a popular solution for salaried individuals in India seeking instant personal loans. With a rating of 3.9 stars and over 5 lakh downloads on the Google Play Store, Instant Mudra promises a seamless, 100% digital loan application process, quick approvals, and disbursements within hours. But is it as reliable and user-friendly as it claims? In this comprehensive Instant Mudra Loan App review, we’ll dive into its features, eligibility criteria, loan terms, customer feedback, and potential drawbacks to help you decide if it’s the right choice for your financial needs.

Instant Mudra, operated by Chintamani Finlease Limited, is a mobile-based financial technology platform that offers instant personal loans in India. The app targets salaried individuals facing short-term financial crunches, providing loans ranging from ₹3,000 to ₹30,000. With a motto of “Our Principle is in Building Good Relationships,” Instant Mudra aims to simplify the borrowing process by eliminating tedious paperwork and long bank queues.

The app is designed to cater to the urgent financial needs of young professionals and salaried individuals, offering a 100% online process, quick approvals, and direct bank transfers. Instant Mudra operates as a Non-Banking Financial Company (NBFC) and collaborates with lending partners to disburse loans. Its user-friendly interface and promise of hassle-free borrowing have made it a go-to choice for many, but customer reviews reveal a mixed experience.

Instant Mudra stands out for its streamlined approach to personal loans. Here are the key features that make it appealing:

High Loan Amount: Borrow between ₹3,000 and ₹30,000, ideal for small, urgent expenses like medical bills, travel, or monthly cash shortages.

100% Online Process: The entire loan application process is digital, from registration to document submission and approval.

Quick Approvals: Loans are approved within 5-48 hours, ensuring funds are available when you need them most.

Collateral-Free Loans: No need to pledge assets or provide security, making it accessible to a wide range of borrowers.

Flexible Tenure: Loan repayment terms range from 3 months to 24 months, allowing borrowers to choose a plan that suits their financial situation.

Low Documentation: Minimal paperwork, requiring only basic documents like a selfie, Aadhaar/PAN card, salary slips, and bank statements.

Credit Score-Based Lending: Loans are granted based on a comprehensive credit score, making it accessible even for those with lower CIBIL scores.

No Hidden Charges: Transparent fee structure with a one-time processing fee (up to 5% of the loan amount plus GST) and a maximum APR of 23%.

These features position Instant Mudra as a convenient option for those seeking instant personal loans online in India. However, the app’s performance and customer satisfaction vary, as we’ll explore later.

Eligibility Criteria for Instant Mudra Loan

To qualify for a loan through Instant Mudra, applicants must meet the following criteria:

Citizenship: Must be an Indian citizen.

Age: 21 years or older.

Income: Minimum monthly salary of ₹25,000.

Bank Account: One active bank account.

Contact: A working phone number.

These requirements are straightforward, making the app accessible to a large segment of salaried professionals. However, the app currently serves only salaried individuals, with plans to expand to other categories in the future.

The documentation process is minimal, aligning with the app’s promise of a hassle-free experience. You’ll need:

Photograph: A selfie.

Income Proof: Last 3 months’ salary slips.

Bank Statement: Updated 6 months’ bank statements of your salary account.

Employment Proof: Employee ID card and visiting card.

Identity Proof: Aadhaar card or PAN card.

Signature Proof: Banker verification after loan approval.

This minimal documentation ensures that applicants can quickly submit their details and move forward with the loan process.

How Does Instant Mudra Loan App Work?

Applying for a loan through Instant Mudra is simple and can be completed in a few steps:

Download the App: Install the Instant Mudra Personal Loan App from the Google Play Store.

Register: Sign up using your mobile number and verify with an OTP.

Enter Details: Fill in personal and financial details to check your eligibility.

Choose Loan Amount: Select a loan amount between ₹3,000 and ₹30,000.

Upload Documents: Submit the required documents digitally.

Loan Approval: Once approved (within 5-48 hours), the loan amount is credited directly to your bank account.

The app’s user-friendly interface and quick processing make it an attractive option for those needing instant loans in India.

Loan Amount, Tenure, Fees, and Charges

Here’s a breakdown of the financial aspects of borrowing from Instant Mudra:

Loan Amount: ₹3,000 to ₹30,000.

Loan Tenure:

Minimum: 3 months.

Maximum: 24 months (including renewal time).

Interest Rate: Maximum APR of 23%.

Processing Fee: Up to 5% of the loan amount (exclusive of GST).

Hidden Charges: None, as per the app’s claims.

Example Calculation:

If you borrow ₹30,000 at an interest rate of 23% per annum with a processing fee of ₹750 for a 12-month tenure, you’ll repay a total of ₹36,900. This breaks down to a monthly EMI of ₹3,075.

This transparent fee structure is a positive aspect, but some users have reported dissatisfaction with the low loan amounts offered, as we’ll discuss in the customer reviews section.

Customer Reviews: What Are Users Saying?

Customer feedback provides valuable insights into the app’s performance. While Instant Mudra has a respectable 3.9-star rating and over 5 lakh downloads, reviews are mixed, with both positive and negative experiences.

Positive Reviews:

Some users praise the app for its quick disbursements and helpful customer support:

One user mentioned, “Very helpful app. In urgency, got the approval within 1-2 hours and disbursed in account with minimal documents.”

Another user noted, “I am very satisfied with Instant Mudra as it helped me improve my CIBIL score. Staff is polite and cooperative.”

These reviews highlight the app’s ability to deliver on its promise of quick loans and support for users with lower credit scores.

Negative Reviews:

However, several users have reported significant issues, including low loan amounts, poor customer service, and technical glitches:

Reena Parmar (12/03/25): “I had a very bad experience. Rude staff. They asked me too many documents and the loan amount they offered was just 4k… Anuradha’s chats were so bad, she called me ‘sir’ every time and was rude when I asked to close my application.” (65 people found this helpful)

Raj Venati (12/04/25): “Worst app, don’t waste your time. They took nearly 3 days and only approved ₹3,000. You’ll get frustrated with their late responses.”

Pushpendar Kumar (18/03/25): “Very bad services. They asked for documents but stopped responding after I submitted them. Totally fake promises.”

Anil Kumar Reddy (24/03/25): “Waste app. Good for ₹1,000-₹4,000, but for higher amounts, you need to repay for 4-5 years to qualify for ₹30,000.”

Ketan Mandlik (15/04/25): “They signed documents on my behalf, and I still haven’t received my loan. No one is responding.”

Deepak Singh (01/03/25): “Poor application. Loan payment done, but support team doesn’t update the status automatically.”

Raja Tripathi (13/04/25): “Absurd app. It gets stuck after the welcome page.”

Lucky Lucky (28/02/24): “After collecting all my data, the app got stuck, and it’s been 3 days with no response. Worst experience.”

These reviews highlight recurring issues such as low loan approvals, unresponsive customer support, technical glitches, and rude staff behavior. The app’s inability to approve higher loan amounts for new users is a common complaint, with some users feeling misled by the promise of up to ₹30,000.

Pros and Cons of Instant Mudra Loan App

Pros:

Quick and Easy Process: 100% online application with minimal documentation.

Fast Disbursements: Loans credited within 5-48 hours.

Collateral-Free: No need for assets or security.

Transparent Fees: No hidden charges, with a clear breakdown of interest and processing fees.

Low CIBIL Funding: Suitable for users with lower credit scores.

Cons:

Low Loan Amounts: Many users report being approved for only ₹3,000-₹4,000, far below the advertised ₹30,000.

Poor Customer Support: Complaints about rude staff and unresponsive teams.

Technical Issues: App glitches, such as getting stuck on the home page or failing to update loan status.

Limited Eligibility: Only available to salaried individuals with a minimum income of ₹25,000.

Mixed Reputation: Negative reviews raise concerns about reliability and professionalism.

Is Instant Mudra Loan App Safe and Legit?

Instant Mudra is operated by Chintamani Finlease Limited, a registered NBFC, which lends credibility to its operations. The app is available on the Google Play Store and has a significant user base, indicating a level of legitimacy. However, concerns arise from customer reviews and a 2022 article by Wisdom Ganga, which flagged Instant Mudra for unethical practices, such as:

Approving loans without user consent.

Harassing customers for repayments, including cyberbullying.

Collecting excessive personal data (camera, contacts, SMS, etc.) through broad app permissions.

The article also noted that Instant Mudra lacks transparency about its ownership and NBFC partners, raising red flags about its operations. While the app is not necessarily a scam, these concerns suggest caution. Users should carefully review the app’s privacy policy and permissions before applying.

How Does Instant Mudra Compare to Other Loan Apps?

To provide a balanced perspective, let’s compare Instant Mudra with other popular loan apps in India, such as My Mudra, KreditBee, and MoneyView:

Loan Amount: Instant Mudra offers ₹3,000-₹30,000, while My Mudra provides up to ₹50 lakh, and KreditBee and MoneyView offer up to ₹5 lakh.

Interest Rates: Instant Mudra’s maximum APR is 23%, compared to My Mudra’s 9.99%-24%, KreditBee’s 15%-29%, and MoneyView’s 16%-39%.

Eligibility: Instant Mudra requires a minimum salary of ₹25,000, which is higher than KreditBee (₹10,000) and MoneyView (₹13,500).

Customer Support: My Mudra and MoneyView have better reputations for responsive support, while Instant Mudra struggles with complaints about rudeness and delays.

Approval Time: All apps promise approvals within 24-48 hours, but Instant Mudra’s actual approval amounts are often lower than advertised.

For users needing higher loan amounts or better customer service, alternatives like My Mudra or KreditBee may be more suitable. However, for small, urgent loans, Instant Mudra remains a viable option despite its drawbacks.

Tips for Using Instant Mudra Loan App

If you decide to use Instant Mudra, here are some tips to ensure a smooth experience:

Check Eligibility First: Verify that you meet the income and age criteria to avoid rejection.

Read the Fine Print: Review the loan terms, interest rates, and processing fees before signing.

Limit Permissions: Be cautious about granting excessive app permissions (e.g., access to contacts or SMS).

Contact Support Early: If you face issues, reach out to info@instantmudra.com promptly.

Repay on Time: Timely repayments can improve your CIBIL score and eligibility for higher loan amounts.

Start Small: Given the low approval amounts for new users, apply for a smaller loan to build trust with the app.

Conclusion: Should You Use Instant Mudra Loan App?

The Instant Mudra Loan App offers a convenient solution for salaried individuals seeking instant personal loans in India. Its 100% online process, quick approvals, and collateral-free loans make it appealing for small, urgent financial needs. However, the app’s low loan approval amounts, technical glitches, and poor customer support are significant drawbacks that cannot be ignored. Negative reviews, such as those from Reena Parmar and Raj Venati, highlight issues with rude staff, unresponsive teams, and misleading promises about loan amounts.

For those needing loans below ₹5,000 with minimal documentation, Instant Mudra can be a quick fix, especially if you have a lower CIBIL score. However, if you require higher amounts or a more reliable experience, consider alternatives like My Mudra, KreditBee, or MoneyView. Always weigh the pros and cons, read user reviews, and proceed with caution when sharing personal data.

If you’ve used Instant Mudra, share your experience in the comments below! For more information or to apply, visit the Instant Mudra website or download the app from the Google Play Store.

In the digital lending era, instant loan apps promise quick cash with minimal hassle, but not all are trustworthy. ProtopFin Loan App has gained attention for its bold claims of seamless, transparent, and secure loans. However, recent customer reviews and investigations reveal a darker side, labeling it a 7-day fake loan app with high interest rates, hidden charges, and questionable practices. This ProtopFin Loan App review dives deep into its features, customer complaints, red flags, and why it was removed from the Play Store. With 1500 words of detailed analysis, we’ll cover all searchable keywords to help you make an informed decision and rank this article at the top. Let’s explore whether ProtopFin is a legitimate lender or a fraudulent loan app scam.

{“remix_data”}]}}

What Is ProtopFin Loan App?

ProtopFin is a digital loan facilitation platform operated by Protop Consultancy Services Private Limited. It claims to connect users with JADS Services Private Limited, an RBI-registered NBFC, offering personal loans ranging from ₹2,000 to ₹60,000 with tenures of 90 to 120 days. The app markets itself as a quick loan app with a seamless, transparent, and secure borrowing experience, boasting a 4.3-star rating and 50,000 downloads on the Play Store before its removal.

However, a closer look at user experiences, such as a scathing review by Raunak Alam on March 15, 2025, paints a different picture. Raunak called ProtopFin a “total fraud app”, alleging that for a ₹1,000 loan, only ₹617 was credited to his account, with a ₹1,006 repayment due in just 7 days. This discrepancy, coupled with hidden fees and lack of transparency, raises serious doubts about its legitimacy. The app’s removal from the Google Play Store further fuels suspicions of it being a fake loan app.

Why Was ProtopFin Removed from the Play Store?

The Google Play Store has strict policies for loan apps, prohibiting those with short-term loans (less than 60 days) or exorbitant interest rates. ProtopFin’s 7-day loan terms and high charges likely violated these guidelines, leading to its removal. Additionally, user complaints about fake ratings, hidden deductions, and harassment may have prompted Google to act. This aligns with Google’s 2023 crackdown on SpyLoan apps, which removed 17 fraudulent apps with over 12 million downloads for similar deceptive practices.

The removal is a red flag for users searching for safe loan apps in India. It suggests that ProtopFin failed to comply with RBI regulations or Google’s policies, reinforcing claims that it’s a 7-day fake loan app designed to trap vulnerable borrowers with high interest rates and short repayment periods.

ProtopFin Loan App: Features and Claims

Before diving into the controversies, let’s examine what ProtopFin claims to offer:

Loan Amount: ₹2,000 to ₹60,000

Tenure: 90 to 120 days (though users report 7-day loans)

Interest Rates: Not clearly disclosed in the app’s description

Processing Fees: Claimed to be transparent but users report hidden charges

Eligibility: Basic KYC documents like Aadhaar, PAN, and bank details

NBFC Partner: JADS Services Private Limited (RBI-registered, but verification needed)

App Rating: 4.3 stars with 50,000 downloads (suspected to be fake)

While these features sound appealing, customer reviews and analysis reveal discrepancies, such as short-term loans, high deductions, and lack of transparency, which are hallmarks of fake loan apps in India.

Customer Complaints: The Shocking Truth

The most damning evidence against ProtopFin comes from user reviews, particularly Raunak Alam’s experience. Here’s a breakdown of his complaint:

Loan Amount: Applied for ₹1,000, received only ₹617

Deductions: ₹383 was deducted upfront without prior disclosure

Repayment: ₹1,006 due in 7 days, implying an exorbitant interest rate

Transparency: No clear details on deductions or charges before loan disbursal

Rating: Called the app “wahiyat” (terrible) and warned others to avoid it

Raunak’s review highlights hidden fees, short repayment terms, and misleading practices, which are common tactics of fraudulent loan apps. Other users have echoed similar sentiments, reporting harassment through calls, texts, and threats when unable to repay on time. These patterns align with characteristics of SpyLoan apps, which collect sensitive data and blackmail users.

Red Flags of ProtopFin Loan App

Here are the key warning signs that ProtopFin may be a fake loan app:

Hidden Fees: Significant upfront deductions (e.g., ₹383 on a ₹1,000 loan) not disclosed beforehand.

High Interest Rates: The 7-day repayment of ₹1,006 for a ₹617 loan suggests an APR far exceeding RBI caps (typically 36% for personal loans).

Fake Ratings: The 4.3-star rating may be manipulated, as seen in other scam apps with inflated reviews.

Lack of RBI Verification: While ProtopFin claims to partner with JADS Services, users must verify this NBFC’s registration on the RBI website.

Harassment Tactics: Users report aggressive recovery methods, including threats and contact list access, a common trait of fake loan apps.

Play Store Removal: Its removal from the Google Play Store indicates non-compliance with lending regulations.

These red flags make ProtopFin a risky choice for anyone seeking an instant loan app in India.

How ProtopFin Compares to Other Fake Loan Apps

ProtopFin’s practices mirror those of other fraudulent loan apps identified in India, such as Agile Loan, Angel Loan, and Quick Cash. These apps often:

Promise instant loans with no credit checks or minimal documentation

Charge exorbitant interest rates (sometimes over 50% for 7 days)

Deduct upfront fees before disbursing funds

Use harassment tactics like calling contacts or sending fake legal notices

Lack RBI registration or transparency about terms

Unlike RBI-approved loan apps like Fibe, Hero FinCorp, or Bajaj Finserv, which offer transparent terms, competitive interest rates (9-36% APR), and longer tenures, ProtopFin’s 7-day loan scam targets vulnerable borrowers, trapping them in a debt cycle.

How to Identify a Fake Loan App Like ProtopFin

To avoid falling prey to apps like ProtopFin, watch for these signs:

RBI Registration: Verify the app’s NBFC or bank partner on the RBI website (sachet.rbi.org.in).

Transparent Terms: Genuine apps provide clear details on interest rates, fees, and repayment terms upfront.

User Reviews: Check for patterns of complaints about hidden charges, harassment, or short-term loans.

Permissions: Avoid apps requesting unnecessary access to contacts, photos, or messages.

Upfront Fees: Legitimate lenders deduct fees after loan approval, not before disbursal.

Play Store Presence: Apps removed from the Google Play Store are often fraudulent.

By following these tips, you can steer clear of fake loan apps in India and choose safe loan apps like NoBroker Insta Cash or MoneyView.

What to Do If You’ve Used ProtopFin

If you’ve already borrowed from ProtopFin or suspect you’ve been scammed:

Stop Payments: Avoid paying additional fees or repaying if the app is fraudulent.

Secure Your Data: Change passwords and monitor your bank accounts for unauthorized transactions.

Report to Authorities: File a complaint with the RBI Sachet portal, cybercrime portal, or local police.

Check CIBIL: Fake apps can’t report to credit bureaus, but verify your CIBIL score to ensure no damage.

Warn Others: Share your experience on social media or review platforms to alert potential victims.

Why You Should Avoid ProtopFin Loan App

ProtopFin’s 7-day loan scam, high interest rates, hidden charges, and Play Store removal make it an unreliable and risky choice. Its practices align with fake loan apps that exploit borrowers with urgent financial needs. Instead, opt for RBI-registered loan apps like Fibe, Hero FinCorp, or Bajaj Finserv, which offer transparent loans, competitive rates, and longer repayment terms.

With no obligation to repay a fraudulent loan app, users can protect their finances by avoiding ProtopFin and reporting its activities. Stay cautious, verify lenders, and prioritize safe instant loan apps for your financial needs.

FAQs About ProtopFin Loan App

Q1: Is ProtopFin Loan App safe to use? A: No, ProtopFin is considered a fake loan app due to its hidden fees, high interest rates, 7-day loan terms, and Play Store removal. User complaints and lack of transparency further confirm its risks.

Q2: Why was ProtopFin removed from the Play Store? A: ProtopFin likely violated Google Play Store policies by offering 7-day loans and charging exorbitant interest rates, leading to its removal. User complaints about fraudulent practices may have also contributed.

Q3: Does ProtopFin charge high interest rates? A: Yes, user reviews indicate high interest rates, with a ₹1,000 loan requiring ₹1,006 repayment in 7 days, implying an APR far above RBI caps.

Q4: Is ProtopFin registered with the RBI? A: ProtopFin claims to partner with JADS Services, an RBI-registered NBFC, but users must verify this on the RBI website. Lack of clear documentation raises doubts.

Q5: What should I do if I’ve taken a loan from ProtopFin? A: Stop payments, secure your bank accounts, report the app to the RBI Sachet portal or cybercrime authorities, and check your CIBIL score for any impact.

Q6: Are there safe alternatives to ProtopFin? A: Yes, opt for RBI-approved loan apps like Fibe, Hero FinCorp, Bajaj Finserv, or NoBroker Insta Cash, which offer transparent terms and competitive rates.

Conclusion

The ProtopFin Loan App markets itself as a quick loan solution, but its 7-day fake loan scam, high interest rates, hidden charges, and Play Store removal expose it as a fraudulent app. User reviews, such as Raunak Alam’s, highlight its lack of transparency and harassment tactics, making it a risky choice for borrowers. By choosing RBI-registered loan apps and following our tips to identify fake loan apps, you can protect your finances and avoid scams. Stay informed, verify lenders, and borrow responsibly to ensure a safe loan experience in 2025.!

Bhai, aaj baat karte hain PP Loan App ki, jo ek aisi loan app hai jo sunne mein toh badi simple lagti hai, lekin asal mein iska khel thoda alag hai. Ye app short-term loan ka jadoo toh dikha deti hai, lekin uske sath aata hai ek bada sa interest rate ka bomb! 💣 To chalo, iske bare mein detail mein baat karte hain, aur thodi si awareness bhi failate hain, kyuki yeh app 100% tak interest ek saal ka charge karti hai. Haan, sahi suna, 100%! 😱

PP Loan App ek aisi digital loan platform hai jo chhote-chhote, short-term loans deti hai. Matlab, agar tujhe urgent mein thodi si cash chahiye – jaise 10 din, 15 din, ya zyada se zyada ek mahine ke liye – toh yeh app bolti hai, “Aaja bhai, hum hain na!” Lekin yahan catch hai. Ye loan jaldi milta toh hai, par wapas karne ka time bhi utna hi tight, aur interest rates? Wo toh dil se “uff” nikalwa dete hain.

Iske interface ki baat kare toh, bilkul uss Paise Loan App jaisa vibe hai – wahi desi, kaam chalau look. Na koi fancy design, na koi premium feel. Bas ek simple sa app jo bolta hai, “Lo loan, aur jaldi wapas karo.” Lekin yahan thodi si trust issue wali feeling bhi aati hai, kyuki app ka design aur flow thoda dodgy sa lagta hai.

Loan Ka Scene Kya Hai?

PP Loan App ka asli khel hai uske loan terms aur interest rates. Yeh app chhote loans offer karti hai, jo usually 10 din se lekar ek mahine tak ke hote hain. Maan lo, tujhe 5,000 ya 10,000 rupaye chahiye, toh yeh app jhat se process karke paise dal deti hai. Lekin yahan dikkat shuru hoti hai:

Short-Term Loans: Loan ka duration itna chhota hai ki agar tu time pe wapas nahi kar paya, toh late fees aur extra charges ka silsila shuru ho jata hai.

High Interest Rates: Yeh app interest ke naam pe ek saal ka 100% tak charge kar sakti hai. Matlab, agar tune 10,000 ka loan liya, toh ek saal mein 10,000 aur dene pad sakte hain – sirf interest ke! 😵 Ye rate bohot zyada hai, jab compare karo traditional banks ya regulated NBFCs se.

Hidden Charges: Kai baar processing fees ya service charges ke naam pe extra paisa kat jata hai, jo tujhe pehle clearly nahi bataya jata.

Interface Aur Usability

App ka interface koi khas nahi hai, bhai. Bilkul waisa hi hai jaise koi local developer ne jaldi-jaldi bana diya ho. Agar tune Paise Loan App ya koi similar app use kiya hai, toh tujhe familiar sa lagega. Functionality ke mamle mein kaam toh chal jata hai – loan apply karo, documents upload karo, aur paise mil jate hain. Lekin yeh app kisi bhi tarah se polished ya user-friendly nahi hai. Aur haan, thodi si sketchy vibe bhi deti hai, toh sensitive info share karte waqt do baar soch lena.

Kyun Aware Rehna Zaroori Hai?

Ab baat karte hain asli wajah ki – kyun PP Loan App ke sath sambhal ke rehna chahiye. Sabse badi baat, iske interest rates. 100% annual interest rate koi mazak nahi hai! Agar tu short-term ke liye bhi loan le raha hai, toh bhi daily ya monthly basis pe calculate kare toh yeh bohot mehnga padta hai. Dusri baat, short repayment period ki wajah se agar tu repayment miss karta hai, toh late fees aur penalties tujhe aur gehri debt cycle mein dhakel sakte hain.

Aur ek cheez – yeh app regulated platforms jaisa transparent nahi hai. Kai users ne shikayat ki hai ki terms and conditions clearly mention nahi hote, aur kabhi-kabhi extra charges ke bare mein baad mein pata chalta hai. To agar tu financially tight spot mein hai, toh PP Loan App shayad tera best option nahi hai.

PP Loan App ek aisi app hai jo emergency mein kaam toh aati hai, lekin iski mehengi shartein aur sky-high interest rates isse risky banate hain. 100% annual interest rate aur short repayment periods ke sath, yeh app chhote loan ke naam pe bade financial trap mein fasaa sakti hai. Interface bhi koi khas nahi, aur trust factor pe bhi thoda doubt rehta hai.

Toh mera advice? Agar tujhe sach mein urgent paise chahiye, toh pehle regulated aur transparent platforms explore kar. PP Loan App ko last resort hi rakho, aur agar use karna bhi pade, toh terms and conditions dhyan se padh lena. Paise ka jugad karna zaroori hai, lekin apne pocket ka bhi khayal rakhna, bhai! 😎

Kya bolta hai, koi aur loan app ke bare mein janna hai? Ya ispe koi aur sawal? Comment mein bata! 👇

Looking for a quick and reliable solution to meet your urgent financial needs? PayRupik, an instant personal loan app, claims to be your “best friend” for hassle-free borrowing. In this SEO-friendly review, we’ll dive into PayRupik’s features, eligibility, loan details, customer feedback, and whether it lives up to its promises. Let’s explore if PayRupik is the right online loan app for you.

PayRupik is an online instant personal loan platform by Sayyam Investments Pvt Ltd, a registered NBFC under the RBI. Trusted by over 5 million users, it offers quick cash loans ranging from ₹1,000 to ₹20,000 with a fully digital process. PayRupik emphasizes transparency, speed, and security, disbursing funds directly to your bank account in as little as 15 minutes.

Key Features of PayRupik:

Loan Amount: ₹1,000 to ₹20,000

Loan Tenure: 91 days to 365 days

Interest Rate: Up to 35% APR

Processing Fee: ₹80 to ₹2,000 (plus 18% GST)

100% Online Process: No paperwork, fully digital application

Security: Data transferred via secure HTTPS connection

Disbursal Time: Funds credited within 15 minutes

How Does PayRupik Work?

PayRupik’s process is designed to be fast and user-friendly. Here’s how to get started:

Download the App: Install the PayRupik app from the Google Play Store or Apple App Store.

Create an Account: Sign up with basic details.

Upload KYC Documents: Submit ID proof, address proof, and PAN card.

Apply for a Loan: Choose your loan amount and tenure, and get instant approval.

Receive Funds: Approved loans are disbursed to your bank account within minutes.

Eligibility Criteria:

Indian citizen

Age: 18+ years

Steady monthly income

Minimum annual household income: ₹3,00,000

PayRupik Loan Example

To understand the costs, let’s look at a representative example provided by PayRupik:

Loan Amount: ₹6,000

Tenure: 120 days

Interest Rate: 25% per annum

Interest Payable: ₹493

Processing Fee: ₹100

GST (18%): ₹18

Total Repayment: ₹6,611

APR: 30.97%

This breakdown highlights PayRupik’s transparency in displaying all charges upfront, helping users make informed decisions.

Why Choose PayRupik?

PayRupik markets itself as a reliable and efficient loan app with several benefits:

Transparency: As an RBI-registered NBFC, PayRupik ensures clear terms and no hidden charges.

Instant Disbursal: Get funds in your account within 15 minutes, ideal for emergencies.

No Paperwork: The 100% online process eliminates the need for physical documents.

Data Security: Your personal information is protected with secure HTTPS encryption.

Flexible Tenure: Choose repayment periods from 91 days to 1 year.

Customer Reviews: What Are Users Saying?

While PayRupik boasts impressive features, customer reviews reveal mixed experiences. Here’s a summary of feedback from users:

Positive Feedback:

Quick Disbursal: Users like Ansh Panjwani appreciate the app’s fast loan disbursal process, making it convenient for urgent needs.

User-Friendly App: The digital application process is straightforward and efficient for many.

Negative Feedback:

Poor Customer Service: Multiple users, including Surendra Kumar and MUSHTHAQ KT, report unprofessional and unresponsive customer support. Issues like login problems and EMI repayment remain unresolved.

High Interest Rates: Nirbhay Shukla and others criticize the high interest rates and steep late fees, which can negatively impact CIBIL scores.

Loan Rejections: Surendra Kumar notes frequent loan rejections without clear reasons, even for users with timely repayments.

Harassment for Repayments: Users complain about excessive calls and harassment before repayment due dates.

Delayed or Failed Disbursals: Meta Tron highlights instances where confirmed loans were not credited, with no support from the team.

Common Complaints:

Unresponsive customer care (email: service@payrupikloan.in, phone: 0224-8930118)

High interest rates and fees

Technical issues with the app, such as login failures

Aggressive collection practices

Pros and Cons of PayRupik

Pros:

Fast and easy loan application process

Instant disbursal within 15 minutes

Transparent fee structure

Secure data handling

RBI-registered NBFC for credibility

Cons:

High interest rates (up to 35% APR)

Poor customer service responsiveness

Frequent loan rejections without explanation

Technical glitches in the app

Aggressive repayment reminders

Is PayRupik Safe and Legit?

Yes, PayRupik is a legitimate loan app operated by Sayyam Investments Pvt Ltd, an RBI-registered NBFC. It uses secure HTTPS connections to protect user data and complies with Indian financial regulations. However, user reviews suggest caution due to high interest rates, poor customer support, and aggressive repayment practices.

Should You Use PayRupik?

PayRupik is a viable option for those needing quick cash loans with minimal paperwork, especially for small amounts (₹1,000–₹20,000). Its fast disbursal and transparent terms are strong points. However, high interest rates, unreliable customer support, and negative user experiences raise red flags.

Our Recommendation:

Consider PayRupik if you need an instant loan and can repay on time to avoid late fees and CIBIL score impacts.

Explore Alternatives like Cred, MoneyTap, or KreditBee, which may offer better customer service and lower rates.

Read Terms Carefully: Understand the interest rates, fees, and repayment schedule before applying.

PayRupik offers a convenient solution for instant personal loans, but its high interest rates, poor customer service, and technical issues may outweigh the benefits for some users. Weigh the pros and cons, read user reviews, and compare with other loan apps before deciding.

Have you used PayRupik? Share your experience in the comments below to help others make an informed choice!

हाल ही में गूगल प्ले स्टोर पर एक नई लोन ऐप “Creditrack Credit Assistant” लॉन्च हुई है, जो दावा करती है कि यह आपके क्रेडिट स्कोर को बढ़ाने में मदद करेगी। लेकिन क्या यह वाकई आपकी फाइनेंशियल हेल्प के लिए बनी है, या फिर यह एक छिपा हुआ ठगी का जाल है? यूजर्स के अनुभव और इस ऐप की कार्यप्रणाली को देखते हुए यह साफ होता है कि यह एक शॉर्ट-टर्म लोन ऐप है, जो हाई इंटरेस्ट रेट्स के साथ लोगों को फंसाने का काम कर रही है। आइए, इस ऐप की हकीकत को गहराई से समझते हैं और जानते हैं कि आपको इससे क्यों सावधान रहना चाहिए।

Creditrack Credit Assistant क्या है?

Creditrack Credit Assistant अपने आप को एक क्रेडिट स्कोर सुधारने वाली सर्विस के रूप में पेश करती है। यह यूजर्स को लुभाने के लिए आकर्षक वादे करती है, जैसे कि आसान लोन अप्रूवल और क्रेडिट स्कोर में सुधार। लेकिन असल में यह एक 7-दिन की अवधि वाला लोन प्रोवाइड करती है, जिसमें बेहद ऊंची ब्याज दरें और छिपे हुए चार्जेस शामिल हैं। यूजर्स का कहना है कि यह ऐप उनके फाइनेंशियल हेल्थ को बेहतर करने के बजाय उन्हें कर्ज के जाल में फंसा रही है।

यूजर्स का अनुभव: ठगी का खुलासा

एक यूजर ने अपना अनुभव साझा करते हुए बताया कि उसे 5000 रुपये का लोन अप्रूव हुआ, लेकिन उसके अकाउंट में सिर्फ 2700 रुपये जमा हुए। इसके बाद, मात्र 7 दिनों में उसे 5200 रुपये चुकाने के लिए कहा गया। इसका मतलब है कि 2700 रुपये पर 7 दिनों में लगभग 92% का ब्याज वसूला जा रहा है, जो कि किसी भी वैध फाइनेंशियल इंस्टीट्यूशन के मानकों से कहीं ज्यादा है। यह साफ संकेत है कि Creditrack Credit Assistant पारदर्शी लोन सर्विस देने के बजाय लोगों को लूटने का जरिया बन रही है।

क्या यह RBI रजिस्टर्ड NBFC के साथ काम करती है?

भारत में कोई भी वैध लोन ऐप जो लोन प्रोवाइड करती है, उसे रिजर्व बैंक ऑफ इंडिया (RBI) के दिशा-निर्देशों का पालन करना होता है और किसी रजिस्टर्ड नॉन-बैंकिंग फाइनेंशियल कंपनी (NBFC) के साथ पार्टनरशिप में काम करना जरूरी होता है। लेकिन Creditrack Credit Assistant के बारे में कोई ठोस जानकारी उपलब्ध नहीं है जो यह साबित करे कि यह RBI से मान्यता प्राप्त NBFC के साथ जुड़ी है। बिना रजिस्ट्रेशन के काम करने वाली ऐसी ऐप्स अक्सर फर्जी होती हैं और यूजर्स को ठगने के लिए डिज़ाइन की जाती हैं।

कैसे पहचानें कि यह फ्रॉड ऐप है?

Creditrack Credit Assistant जैसी ऐप्स से बचने के लिए कुछ लाल झंडों (Red Flags) पर ध्यान देना जरूरी है:

हाई इंटरेस्ट रेट्स और छिपे हुए चार्जेस: वैध लोन ऐप्स पारदर्शी तरीके से ब्याज दरें और फीस बताती हैं। लेकिन इस ऐप में लोन की राशि का बड़ा हिस्सा काट लिया जाता है और फिर भारी ब्याज वसूला जाता है।

शॉर्ट-टर्म लोन की मजबूरी: 7 दिनों जैसे बेहद कम समय में पूरा भुगतान करने का दबाव यूजर्स को कर्ज के चक्र में फंसाता है।

RBI रजिस्ट्रेशन की कमी: अगर कोई ऐप अपने NBFC पार्टनर या RBI रजिस्ट्रेशन की जानकारी साफ तौर पर नहीं देती, तो यह संदिग्ध है।

अनचाही परमिशन: कई फर्जी ऐप्स आपके फोन के कॉन्टैक्ट्स, गैलरी और डेटा तक पहुंच मांगती हैं, जिसका इस्तेमाल बाद में ब्लैकमेलिंग के लिए हो सकता है।

पॉजिटिव रिव्यूज पर शक: प्ले स्टोर पर ढेर सारे 5-स्टार रिव्यूज फर्जी हो सकते हैं, जो यूजर्स को भ्रमित करने के लिए डाले जाते हैं।

फर्जी लोन ऐप्स से होने वाले नुकसान

Creditrack Credit Assistant जैसी अनरजिस्टर्ड ऐप्स से लोन लेना आपके लिए कई जोखिम पैदा कर सकता है:

फाइनेंशियल लॉस: ऊंची ब्याज दरों और छिपे चार्जेस की वजह से आप जरूरत से ज्यादा पैसे चुकाते हैं।

डेटा चोरी: आपकी पर्सनल जानकारी जैसे आधार, पैन और बैंक डिटेल्स का गलत इस्तेमाल हो सकता है।

हरासमेंट: रिपेमेंट न करने पर ये ऐप्स यूजर्स को धमकियां देती हैं और उनके कॉन्टैक्ट्स को परेशान करती हैं।

क्रेडिट स्कोर पर असर: अगर आप समय पर पेमेंट नहीं कर पाते, तो यह आपके क्रेडिट स्कोर को नुकसान पहुंचा सकता है।

क्या करें अगर आप फंस गए हैं?

अगर आपने गलती से Creditrack Credit Assistant Loan App से लोन ले लिया है या ऐसी किसी फर्जी ऐप से परेशान हैं, तो ये कदम उठाएं:

शिकायत दर्ज करें: नेशनल साइबर क्राइम रिपोर्टिंग पोर्टल (cybercrime.gov.in) पर अपनी शिकायत दर्ज करें।

RBI से संपर्क करें: RBI के सachet पोर्टल पर ऐसी ऐप्स की रिपोर्ट करें।

बैंक को सूचित करें: अपने बैंक को तुरंत बताएं और संदिग्ध ट्रांजैक्शंस को ब्लॉक करने के लिए कहें।

कानूनी सलाह लें: किसी वकील से सलाह लेकर अपने अधिकारों की रक्षा करें।

सुरक्षित लोन ऐप्स कैसे चुनें?

हमेशा RBI से रजिस्टर्ड NBFC के साथ काम करने वाली ऐप्स चुनें, जैसे KreditBee, MoneyView या Fibe।

लोन लेने से पहले ऐप की टर्म्स एंड कंडीशंस, ब्याज दरें और रिव्यूज चेक करें।

ऐसी ऐप्स से बचें जो बहुत आसान और तुरंत लोन देने का वादा करती हैं बिना किसी डॉक्यूमेंटेशन के।

निष्कर्ष: सावधानी ही बचाव है

Creditrack Credit Assistant भले ही क्रेडिट स्कोर बढ़ाने का दावा करे, लेकिन इसके पीछे की सच्चाई इसे एक संभावित फ्रॉड ऐप बनाती है। हाई इंटरेस्ट रेट्स, छिपे चार्जेस और RBI रजिस्ट्रेशन की कमी इसे संदिग्ध बनाते हैं। अगर आपको तुरंत पैसों की जरूरत है, तो हमेशा भरोसेमंद और रेगुलेटेड लोन ऐप्स का इस्तेमाल करें। अपनी मेहनत की कमाई और पर्सनल डेटा को सुरक्षित रखने के लिए सावधानी बरतें और ऐसे जाल में न फंसें।